What will your life look like in a year? Five years? Twenty years?

One of the big problems with setting goals, especially financial ones, is that we’re struggle with imagining our future selves.

Remember what you imagined you’d be as an adult when you were a kid. I’m guessing there are some gaps between that dream and your current reality.

When we talk about financial goals, we’re frequently talking about long timeframes.

Consider retirement, for example. That could be upwards of 20 or 30+ years from now (even if you are 60 yrs old like I am… our life expectancy in about 20-25+ more years). Some of you can’t even imagine yourself at that age, let alone plan for it. That’s your parents, not you!

We do the same thing with our children. When our first child is born, college is the last thing on our mind. But by the time we have 2-3 children, we have a good idea how fast 18 years can go by.

When we start talking about our distant future selves, it’s easy to justify the decision to not do anything. In fact, our future selves can often feel like some other annoying person constantly stealing heaps of fun from our current selves.

Even though our future selves may feel like a big old pain in the neck, it’s important to realize that appeasing that person is still very much in our best interest.

What’s the solution?

To start with, we need to get really clear on our goals. And I’m talking broadly. You don’t have to know exactly what college your first-grader is going to go to and exactly what the tuition is going to be. Just don’t pretend that 18 is a long way off. It’s not. So you better start saving now.

You may feel like you’re still 30, but if you just celebrated (or mourned) turning 40, it’s time to get real. Our future selves will be here faster than we think.

Why prepare for the future now? To avoid being a 40, 50 or 60-year-old that wants to hit your 30-something self over the head for doing stupid adult stuff, like not getting clear on your financial goals.

Dave Conley, CFP

Question:

I hear the dollar has been getting stronger, why is this happening and what difference does it make?

Answer:

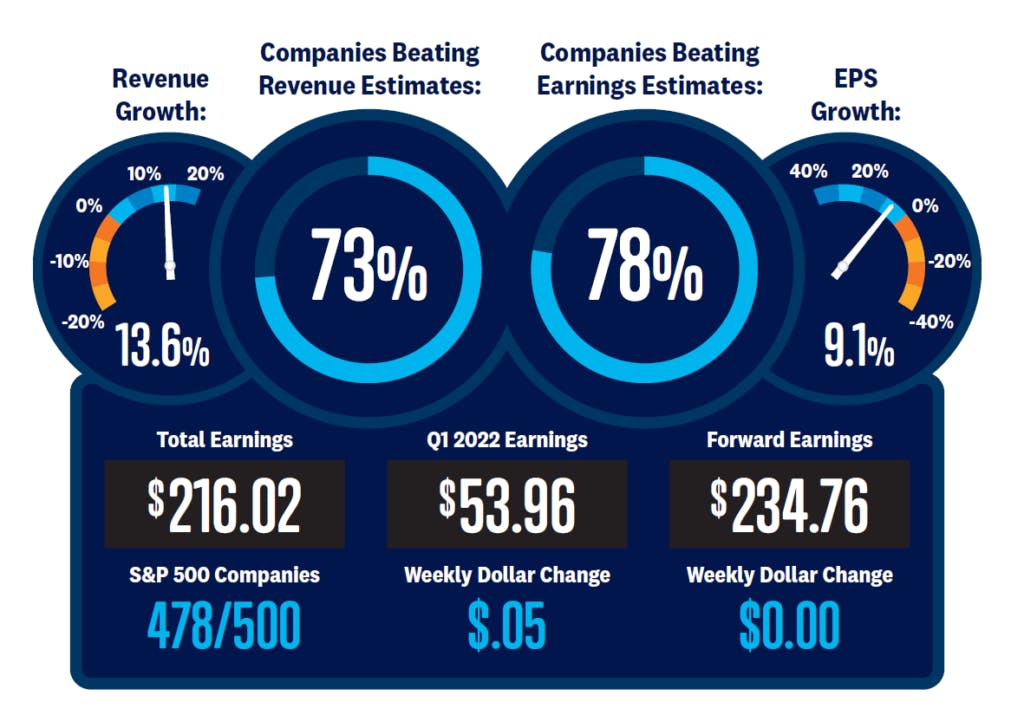

The value of the dollar is soaring (up +18% over the past year). When the price of something surges, it suggests that demand for that thing (in this case US dollars) exceeds the supply. A very strong dollar is a sign of a world that is desperate for a safe haven. For governments, institutions & investors worldwide that safe haven in an uncertain world is United States Dollars. Secondly, a strong dollar makes imported items cheaper for the US consumer and makes traveling abroad less expensive. The negative consequence of a strong dollar is that US companies selling products abroad will find that their products more expensive (hurting sales). Over 40% of S&P 500 company sales are from outside the US.

Bi-Weekly Economic & Market Notes

Recession or no recession?

The market pundits remain intensely focused on the question of whether the U.S. economy is in or about to enter recession. For a long-term investor (someone who will not need all their money in the next 5-6 years) recessions are just part of the investing process. As a rule of thumb, recessions last about 12 months and result in a market decrease (bear market) of about -25%, but the recovery process (bull market) lasts 3-5 years and sees an average increase in stocks of about +114%. Understanding these historical facts helps you to understand why sticking with your investment plan (regardless of current economic conditions) can increase the likelihood of your investments providing the returns you need to reach your financial goals.

Let’s look at some recent economic data:

- Payrolls surged by 528,000 in July and the unemployment rate fell to 3.5%. In addition, the previous two months were revise UP adding another 28,000 jobs to the original estimates. Clearly, these gains further cement the claim that the U.S. is currently not in recession.

- The decline in unemployment and the labor participation rate (the proportion of the working-age population that is either working or actively looking for work) will frustrate central bankers since a tighter labor market adds inflation risk to the economy.

- Stocks & recessions, keep in mind that stocks tend to look forward by four to six months and can provide warnings of changing economic conditions.

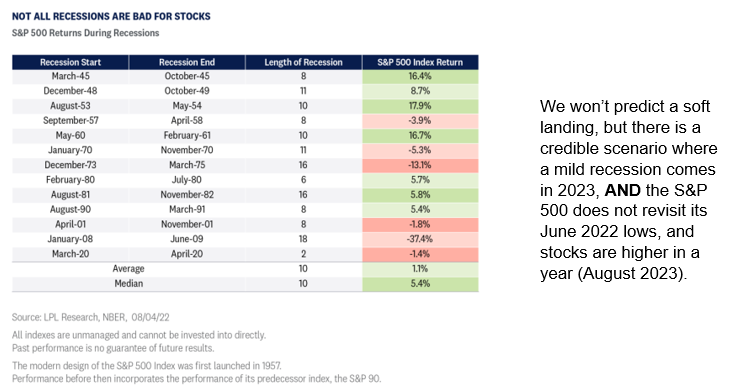

- The entirety of a recession—particularly a mild one—hasn’t historically been all that bad for stocks from start to finish. As shown in the graph below, the median S&P 500 performance during recessions has been positive at 5.4%. (The average of 1.1% is dragged down by 2008- 2009 when the index tumbled 37%). How can this be? As noted before, stocks anticipate both the start and end of recessions several months ahead of time. In particular, the bottom of a recession tends to be followed by powerful rallies before the recession officially ends. By the time the recession is deemed over, the stock market’s recovery is typically well underway.

- The amount of money the average American has to use to pay on their debt (as a % of their income) is near a 30 year low at 9.5% of personal income. This means that contrary to popular belief, the average American is in better shape (debt/income) than before the last five recessions (going back to 1980 the Reagan years).

- Existing home sales fell 5.9% in July, the sixth consecutive month of declines as higher interest rates weigh on housing affordability and prospective buyers. As the housing market slowed, so did prices.

- Although the rate of sales is slowing dramatically, the market is still short on supply of homes. At the current sales rate, it would take roughly three months to clear inventory. As supply remains tight, homes are selling quickly and still at elevated prices. In July, the average existing home for sale was on the market for only 14 days, three days shorter than a year ago.

- The potential risks are the Fed overtightens, consumer incomes fall as the job market weakens, and inflation does not cool as much as the market expects. A slowing housing market could also impact consumer spending through secondary wealth effects.