Before we get started, there is no such thing as “drive-by” tax planning. Personal finance is incredibly personal, and your situation is unique. Rules of thumb can serve as general guidance, but you should always evaluate the full picture before making any decisions. Now, let’s dig into a few Roth conversion rules of thumb that may actually be misconceptions.

Rule of Thumb #1 – You shouldn’t do a Roth conversion if you’re in a high marginal tax bracket.

Before your head explodes, I am not saying everyone in the 37% marginal tax bracket is a candidate for Roth conversions. However, just because you are in a high tax bracket does not automatically mean you should avoid them.

Here are a few reasons why Roth conversions may still make sense:

- Estate tax considerations

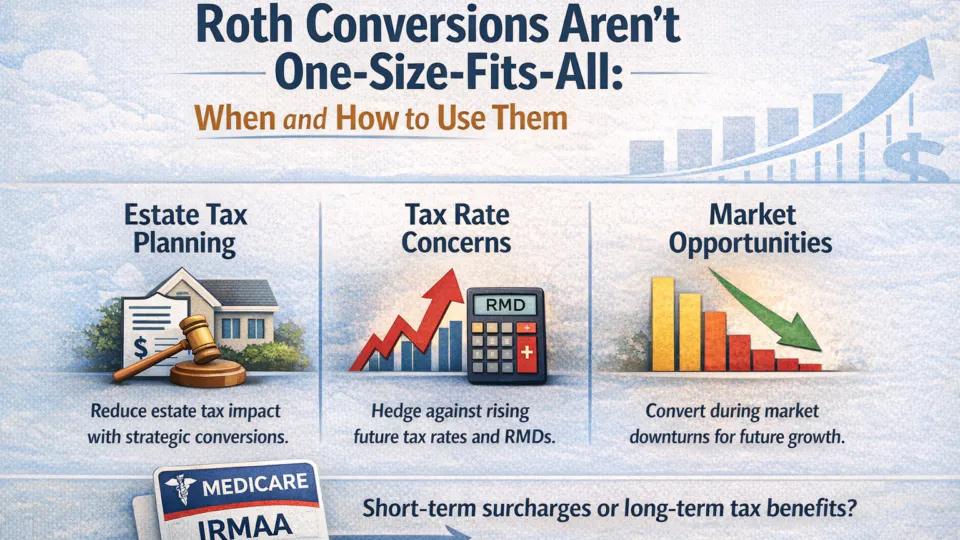

For large estates subject to federal or state estate taxes, Roth conversions can act as a form of tax-efficient gifting. By prepaying income taxes, you move assets out of the estate and into a tax-free Roth account, which is not subject to the federal estate tax rate (up to 40%). - Rising tax rate concerns

If you expect higher future tax rates and anticipate large Required Minimum Distributions (RMDs), converting now—even at a higher bracket—can serve as a hedge against future tax exposure. - Market downturn opportunities

Roth conversions can be more effective when markets are down. Lower account values mean less tax owed on the conversion, positioning those assets for potential tax-free recovery plus growth.

Rule of Thumb #2 – You shouldn’t do a Roth conversion because it will increase your IRMAA surcharge.

What is IRMAA?

The Income-Related Monthly Adjustment Amount (IRMAA) is a surcharge added to Medicare Part B and Part D premiums for higher-income beneficiaries. It is based on a two-year lookback of Modified Adjusted Gross Income (MAGI). For example, 2026 IRMAA surcharges are based on 2024 income.

The key question becomes:

Would you rather pay higher IRMAA surcharges for a year or two now, or risk a decade (or more) of potentially higher surcharges driven by large, uncontrollable RMDs?

This is especially relevant for married couples over RMD age or for surviving spouses who inherit an IRA. While spousal beneficiary IRAs are not subject to the 10-year rule, they are still subject to RMDs based on life expectancy.

Rule of Thumb #3 – Converting to Roth in low tax brackets doesn’t make sense.

Consider a retired couple in the 12% marginal tax bracket with room before reaching the 22% bracket. Some would argue against withdrawing from a traditional IRA if the funds aren’t immediately needed, preferring to defer taxes further into retirement.

However, converting up to the top of the 12% bracket can be a strategic move. It allows for long-term tax-free growth—potentially for decades—while helping manage future tax liability.

Roth conversions aren’t about rules of thumb—they’re about strategy. Without proper planning, you’re guessing. With the right financial advisor, you’re making calculated, coordinated decisions that align with your long-term goals.

If you want to approach this with clarity and confidence, schedule a call HERE or email [email protected].

Securities offered through LPL Financial, Member FINRA/SIPC. Content provided here reflects personal views and has not been reviewed by LPL Financial for accuracy or completeness. The information provided is for informational purposes only, may not be suitable for all investors, and does not constitute personalized financial, tax, investment, or legal advice. All investments involve a degree of risk, including the risk of loss.